NRI Service

Click to know more

about the various NRI client profiles given below:

A. Non resident Indians who have/ intend to have investments in India

B. Non resident Indians who inherit assets in India

C. Non resident Indians/ Non-residents who have / intend to set up a business in India

D. Emigrating Indian/ New NRI

E. Returning NRI

A. Non resident Indians who have/ intend to have investments in India

B. Non resident Indians who inherit assets in India

C. Non resident Indians/ Non-residents who have / intend to set up a business in India

D. Emigrating Indian/ New NRI

E. Returning NRI

Who is NRI?

An Indian abroad is popularly known as

Non-Resident Indian (NRI). NRI status is legally defined under the

Foreign Exchange Management Act, 1999 and the Income-tax Act, 1961 for

applicability of respective laws.

Non-resident under FEMA 1999

Person resident outside India means a person who

is not resident in India.

Person resident in India means

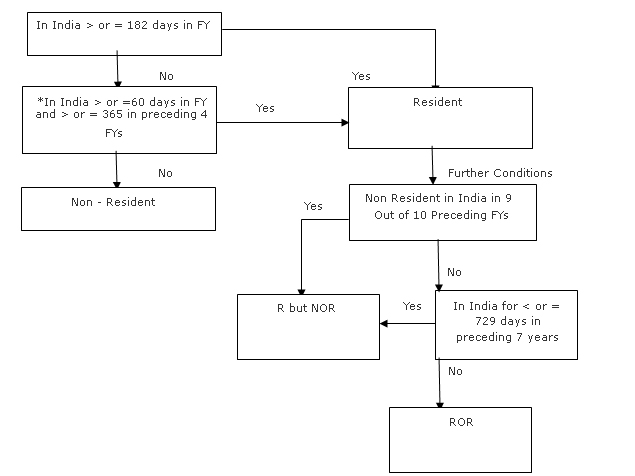

1. A person residing in India for more than one

hundred and eighty-two days during the course of the preceding financial

year but does not include :

3. An office, branch or agency in India owned or controlled by a person resident outside India,

4. An office, branch or agency outside India owned or controlled by a person resident in India;

- A person who has gone out of India or who stays outside

India, in either case

a. For or on taking up employment outside India, or

b. For carrying on outside India a business or vocation outside India, or

c. for any other purpose, in such circumstances as would indicate his intention to stay outside India for an uncertain period; - A person who has come to or stays in India, in either case,

otherwise than

a. For or on taking up employment in India, or

b. For carrying on in India a business or vocation in India, or

c. For any other purpose, in such circumstances as would indicate his intention to stay in India for an uncertain period;

3. An office, branch or agency in India owned or controlled by a person resident outside India,

4. An office, branch or agency outside India owned or controlled by a person resident in India;

Non-resident under Income-tax Act, 1961

We prove various NRI service india like NRI

financial services, NRI legal services.T he term non-resident is

negatively defined under section 6 of the Income-tax Act, 1961. An

individual who is not a resident under the Income-tax Act is a

non-resident. The residential status of an Individual is determined

based on the number of days of stay in India. Financial year (FY) is

April to March.

For the purposes of levy of tax, the Income-tax Act in India has classified the status of an individual assessee into three viz.,

The definition is explained in simple terms as under.

For the purposes of levy of tax, the Income-tax Act in India has classified the status of an individual assessee into three viz.,

- Resident and ordinarily resident (ROR)

- Resident but not ordinarily resident (R but NOR)

- Non-resident (NR)

The definition is explained in simple terms as under.

*Not applicable to a resident going outside

India for employment, a resident who leaves India as a member of crew of

an Indian ship, an Indian citizen or person of Indian origin who is

abroad and comes to India for a visit i.e. if such a person stays in

India for less than 182 days, he would be a non-resident.

In the case of a ROR, his global income is taxed in India. Normally a returning Indian would be assessed as RNOR on his return to India.

In the case of a Non-resident, only the income earned or received in India is taxed in India. Accordingly, income earned outside India by him would not be taxable in India.

India has contracted Double Tax Avoidance Agreements (DTAAs) with various countries. Taxability of Non Resident's Indian income would be decided as per the provisions of these DTAAs. Most of these DTAAs contain provisions for lower rates of tax in case of incomes like dividend, royalties, fees for technical services etc.

In the case of a ROR, his global income is taxed in India. Normally a returning Indian would be assessed as RNOR on his return to India.

In the case of a Non-resident, only the income earned or received in India is taxed in India. Accordingly, income earned outside India by him would not be taxable in India.

India has contracted Double Tax Avoidance Agreements (DTAAs) with various countries. Taxability of Non Resident's Indian income would be decided as per the provisions of these DTAAs. Most of these DTAAs contain provisions for lower rates of tax in case of incomes like dividend, royalties, fees for technical services etc.

Where can we help?

- Determination of your residential status in India

- Interpretation of DTAA with a view to reduce tax liability in India

- Handling of issues relating to inheritance, will, etc.

- Compliances with respect to the Income-tax Act, 1961, Wealth-tax Act, etc.

- Application for Permanent Account Number (PAN)

- Filing of India tax return

- Advising suitable tax saving investments